SSBSS 410-day calving interval

410-day calving interval condition - an assessment of conditional Scottish Suckler Beef Support Scheme payment rates for 2015-2023. The Scottish beef sector has been afforded coupled support payments since 2005. These payments were permitted by the European Union (EU) under the Common Agricultural Policy (CAP) to “types of farming or specific agricultural sectors that are particularly important for economic, social or environmental reasons undergo certain difficulties.” The Scottish Government has announced that there will be 410-day dam calving interval eligibility criteria introduced from 2025 for individual Sottish Suckler Beef Support Scheme (SSBSS) payments. This new condition is aimed to reward technical efficiency, and therefore reduce greenhouse gas emissions associated with poor cow fertility.

This short analytical report to assess what historic calf payment rates would look like under a 410-day calving interval condition was commissioned by the Scottish Government through SRUC’s Underpinning National Capacity – Support for Policy as part of the Scottish Government Environment, Natural Resources and Agriculture 2022-2027 Strategic Research Programme. Using Cattle Tracing System data supplied by the Animal and Plant Health Agency and Scottish Government data supplied by RPID it was possible to estimate the payment rates that would have applied for 2015 – 2023 if the 410-day calving interval had applied over that period.

The analysis highlights that a large proportion of SSBSS claimants had less than 20 eligible calves claimed in 2023. On the islands 21% of businesses had 1-4 eligible calves (1.7% of total calves), and 39% had 1-9 eligible calves (5.2% of total calves). On the mainland 16% of businesses only claimed 1-9 calves, accounting for only 1.2% of calves. In contrast, on the mainland 8.8% of the businesses had claims of 150 and more calves in 2023, accounting for 35% of the claims.

The calving interval performance of the SSBSS Mainland and SSBSS Island herds improved between 2015 and 2023. In 2023, for holdings associated with SSBSS claims, the average non-dairy calving interval performance had improved to 391 days in both the islands and mainland schemes. This shows around a 10-day performance improvement, on average, in a relatively short period of time. Some of this recent improvement was linked to fewer farrow cows being retained during a period of very high cull-cow prices.

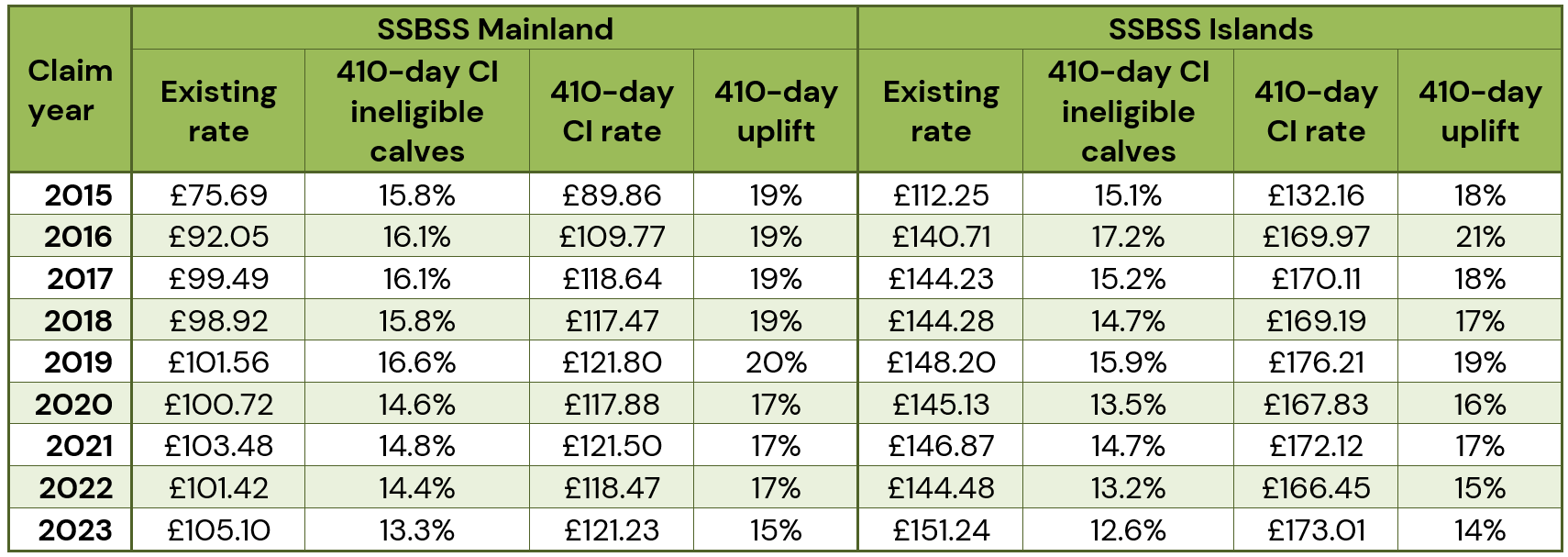

The effects of a 410-day calving interval condition on the 2015 – 2023 SSBSS holdings would have meant an estimated 16.6% to 13.3% of calves in the mainland and between 17.2% to 12.6% of calves on the islands would have been ineligible for support (depending on the year). The reduced number of eligible calves with fixed scheme budgets means that the SSBSS Mainland scheme would have had payment rate uplifts of 15%-20% and the SSBSS Island scheme 14%-21% uplift for eligible calves where the dam had met the 410-day calving interval threshold.

The net business-level effect of the calving interval threshold depends on the interaction between the number of animals meeting the threshold and the higher payment rate: better performing average d businesses could receive uplifts to support payments, and poorer performing businesses would lose. For example, with 100% eligible calves, the average mainland business would gain c.£645 to c.£1000, the average island business c.£350 to c.£740. With only 80% eligible calves, the average funding loss would be c.£325 to c.£455 and c.£170 to c.£470 respectively. With 87% eligible calves, average business-level funding remains essentially constant.