Agri Supply Chain Linkages

Evaluating the significance of agri-supply chains in rural economies: Inter-industry dependency insights from disaggregating UK Input-Output tables

This SRUC report was commissioned by DEFRA and can be downloaded from the link at the bottom of this page or by navigating to https://doi.org/10.58073/SRUC.27930306Report Overview

- The contribution of agriculture in rural economies has changed in the last 30 to 40 years, yet there remains a paucity of evidence on the economic impacts stemming from agricultural activity through its upstream and downstream multipliers - often due to data limitations. This leads to the agricultural sector often being considered separately from other economic activity in rural areas which means its potential role in driving structural change in rural economies is still relatively unknown.

- Backward multipliers can help explain how reliant production in one sector (e.g. dairy farming) is dependent on inputs from other sectors of the economy (e.g. animal feed or veterinary services). In contrast, forward multipliers can illustrate how reliant downstream sectors (e.g. dairy processing) are on the inputs from a specific sector (e.g. dairy farming). These multipliers can be used to assess the relative strength of impacts on the economy from shocks (e.g. trade, market, or support) across UK agri-food sectors.

- The agricultural industry is complex, made up of many specialist sectors, each with unique upstream (e.g. input suppliers) and downstream (e.g. processors) relationships, each with unique capital and labour use intensities. As such, the economic impacts arising from changes in output within different sectors of agriculture can have significantly different wider economic impacts. These differences are lost during aggregation to a single I-O model sector (so-called aggregation bias) which means that the use of ‘agriculture’ multipliers may underestimate or overestimate economic impacts.

- Disaggregating the agriculture sector in the I-O model is, therefore, useful for policy makers and stakeholders. The disaggregated I-O model and associated economic multipliers extend the available toolkits for assessing the economic impacts of policy decisions by providing more nuanced estimates of the strength of forward and backward linkages that the different agricultural sectors have on the economy.

- This disaggregated I-O model allows flows of goods and services into, and out of, sub-sectors of UK agriculture to be assessed across geographies. This includes the indirect impacts along the supply chain (so-called Type I multipliers) and induced expenditure in the wider economy through increased wage expenditure by the workforce (so-called Type II multipliers).

- The UK Input Output (I-O) tables illustrate the strength of inter-industry linkages that arise from economic activity across the United Kingdom. During the first phase of the research, a disaggregated I-O model was developed for Defra that quantified the economic multipliers from agriculture commodity types. This report provides interpretation of the agri-food supply chain interlinkages and assessment of wider economic impacts arising from the model's outputs. The report incorporates other relevant literature and provides estimates of economic multipliers for rural and urban geographies.

Inter Industry Dependencies

- Agriculture may remain a dominant rural industry in terms of registered businesses but has low Gross Value Added (GVA) contributions and is no longer the main source of employment in rural areas. Yet, in some localities, agriculture remains a key component of economic activity, and therefore its upstream and downstream linkages mean the sector likely remains important to the sustainability of some rural economies and communities, particularly in remoter areas where there are fewer employment alternatives. Indeed, many analysts suggest that their greater links between agriculture and local economies exist than can be inferred from traditional statistics.

- Previous research on the spatial distribution of direct, or “first stage”, farm business transactions revealed a highly complex pattern of farm production-related linkages with a large proportion of farmers either trading with their nearest input supplier or output purchaser. Similarly, research examining food and drink business transactions noted relatively localised footprints with some ‘agricultural’ or ‘market’ towns having much greater economic reliance on the farming sector.

- There were strong intra-agriculture flows that reflected the sales of goods and services from one agricultural sector to another. Comparing both crop and livestock coefficients of intersectoral connections it was noticeable that crop outputs had more varied uses in downstream sectors (including within agriculture as feed and bedding for livestock) than livestock products where over 70% of intermediate demand was from the specialised meat and dairy processing sectors. The wider linkages for plant-based products reflect their wide unprocessed use as inputs for food manufacturing whereas most livestock products require abattoir processing as an intermediary stage. The meat processing sector accounted for 70% of intermediate cattle demand and 74% of intermediate sheep demand whilst 78% of downstream intermediate demand from dairy farming was accounted for by dairy processing activities.

- A surprisingly large proportion of rural businesses have been found to have some reliance on the farming sector – but the strength of those relationships and the degree of reliance were highly varied. This reiterates that there are a proportion of businesses with strong upstream and downstream links to farming are more exposed to the market, trade and support conditions surrounding agriculture.

- The unadjusted I-O model for the UK reveals a high degree of heterogeneity in the composition of agri-food sectors across the UK administrations. In 2013 only 44% of the £24bn output generated from products of agriculture, hunting and related services was spent on domestic goods and services (Intermediate Consumption), with 13% spent on imported goods and services, 18% spent on employee wages and contributions with 32% of output being gross operating surplus (profit). Product and production subsidies in agriculture, hunting and related services exceeded taxes paid in the sector meaning there was effectively a negative tax (net subsidy) of the sector that was equivalent to 7% of output (i.e., Common Agricultural Policy support more than tax payments). This contrasted with other agri-food sectors, where gross operating surpluses tended to be lower, and a higher proportion of total output was spent (i) through intersectoral linkages (e.g. 74% of the output in dairy products was spent on intermediate consumption), (ii) on labour (e.g. 31% of output from Bakery and farinaceous products) or (iii) imports (e.g. 35% of vegetable and animal oils and fats output was spent on imports).

Regional specialisation

- The Inter-Departmental Business Register and Total Income from Farming data were used to examine the regional and rural-urban distribution of production by sector and calculate location quotients for use in the I-O model. This spatial analysis revealed the considerable dominance of the English economy in nearly all sectors, with the exceptions of the alcoholic beverages and mining and quarrying sectors where more than half of the UK output came from Scotland. The East of England accounted for 23% of the total UK cereal output, whilst the East of England and Scotland accounted for over half of the total UK output from potatoes. The beef sector was important in Scotland (24% of UK output), Northern Ireland (15%), the South West (15%) and Wales (14%). Yorkshire & the Humber and the East of England nearly accounted for half of the UK pig sector output and the South West (23%) was the most important region for dairy output. Wales (23%) and Scotland (8%) accounted for nearly 40% of UK sheep output – making them exposed to UK-EU future trade conditions for lamb and mutton.

- Many industries associated with the agri-food processing sectors have mixed rural presences. Of the 760 businesses associated with the manufacture of dairy products 53% were located in rural areas, with rural businesses also accounting for 53% of sectoral employment (23,931 across the UK) and half of the £6.9 billion turnover from the sector. However, the preserved meat and meat products sector (£16.2 billion UK turnover and 83,875 jobs) was more urban based, with rural areas only accounting for 43% of the businesses, 35% of the employment and 37% of output.

- In England, across all agricultural sectors, except for cereals, employee wages were the largest upstream outgoing in 2013. Employee wages ranged from £0.213m per £1m output in the pig sector to £0.167m per £1m output in the sheep sector whilst in the cereal sector wages were only £0.141m per £1m output reflecting the sectors’ higher reliance on capital equipment. In cereals capital equipment requires financial borrowing (or lease hire) that is reflected in the strongest upstream link being with the finance, insurance and real estate sector (£0.326m increase in demand per £1m cereal output). The strongest downstream links from the English farming sectors in 2013 were, except for the potato and plant propagation sectors, within intermediate processing sectors. In the potatoes sector, the most important downstream link was with itself – likely reflecting the scale of the seed potato sector as an intra-industry input.

Modelled Multipliers

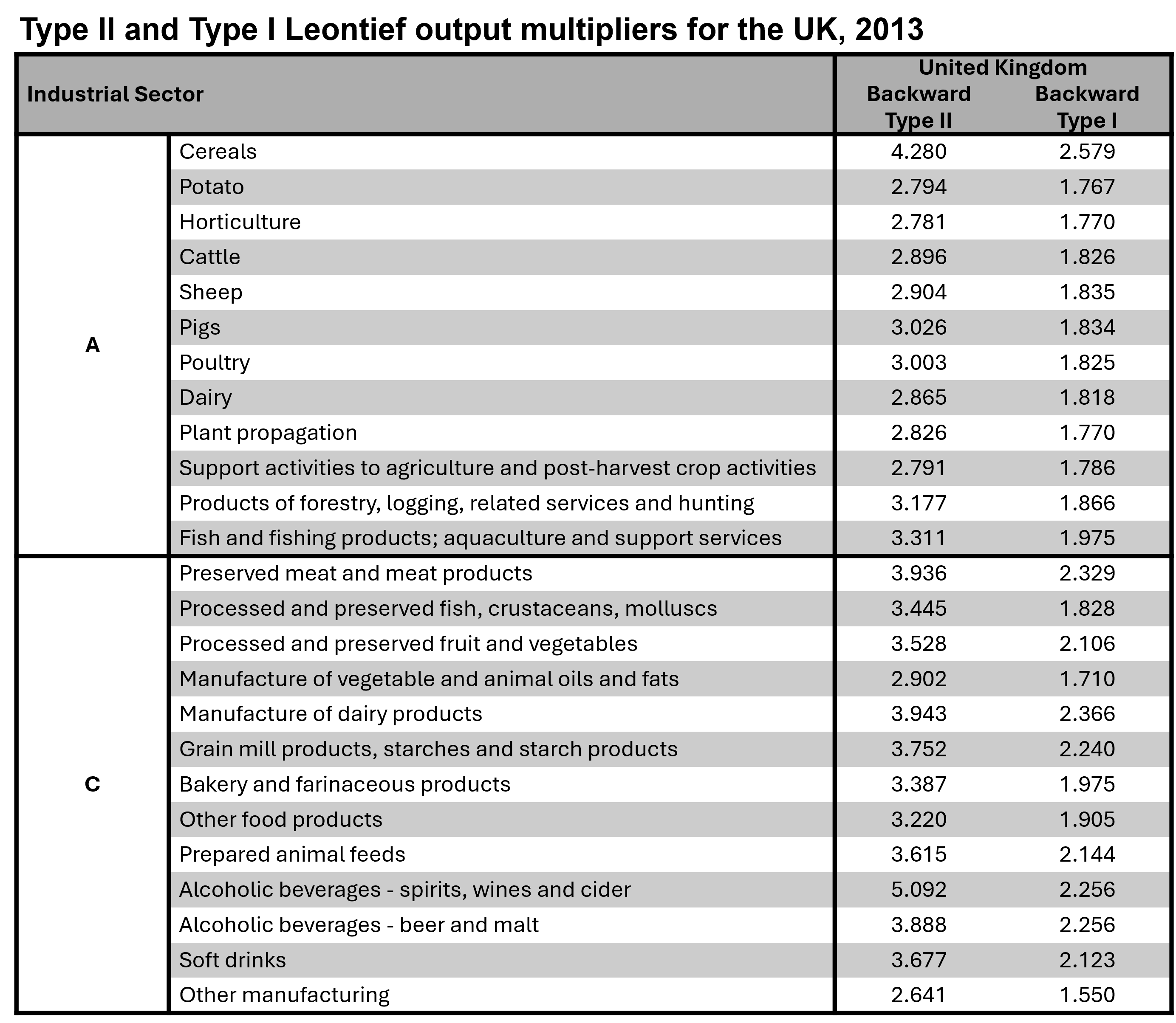

- The estimated output multipliers from the model were generally within the bounds of previous sectoral multiplier studies. Forward multipliers for the cereal sector of 2.05 means that £1 million increase in cereal output would lead to £2.05 million in total economic output with £1 million occurring in the cereal sector (direct effect) and £1.05 elsewhere in the economy (indirect effect). In contrast, the backward multiplier of 2.58 indicates that a £1m increase in final demand for cereals (direct effect) would lead to increased activity along the supply chain to the effect of £1.58m (indirect effect). UK horticulture sector had one of the lowest multipliers in the agriculture sector which likely reflects the sector producing a large amount of product that needs no further added value before household consumption, and labour being a main input that limits intersectoral input effects.

- Most of the food manufacturing sector had higher Type I backward linkages than forward linkages meaning they were more reliant on the upstream sectors for inputs rather than downstream sectors for the sale of goods and services

- When the impact of induced household expenditure was included in the model the Type II output multipliers appeared particularly high for cereals. The UK pig (3.026) and poultry (3.003) Type II output multipliers were also relatively high suggesting a greater reliance on labour input compared to other sectors (such as dairy 2.865). In the pig sector, for example, the model predicted that a £1m increase in final demand for pigs or poultry would lead to £0.8m additional output arising from increased indirect activity with a further £1.17m output from induced impacts across the economy as household spend income on goods and services (these impacts were mirrored for the poultry sector).

- The model estimated that UK-wide Type 1 income multipliers ranged from 1.94 in the pig and poultry sectors (£0.94 indirect income generated from other sectors) to 4.26 in the cereal sector (£3.26 indirect income from other sectors). Again, the cereal sector multiplier appeared high in comparison with the other agricultural sectors - where the second highest income multiplier was 2.17 in the sheep sector. The income multipliers for the UK processing sector range from 1.48 for alcoholic beverages - spirits, wines and cider (only £0.48 indirect income generated from a £1 increase in direct income) to 2.31 for grain mill products, starches and starch products.

- In the UK agriculture sector, the model estimated that plant propagation (3.11) had the highest employment multiplier with the lowest in the pig and poultry sectors (1.31). The Type I employment multiplier for the UK sheep sector was 1.354 meaning that every direct job created in the sheep sector would indirectly create a further 0.354 new jobs in the rest of the economy. Employment multipliers were generally much higher in the food processing sectors, ranging from 1.76 for UK Bakery and farinaceous products to 7.61 for UK grain mill products, starches and starch products.

Conclusions

- This model and report have demonstrated some geographies and upstream and downstream industries that may be impacted by changes to the agriculture sector in the post-EU period. These agricultural shocks may come directly through the market, future trade deals that affect the agri-food sector, or through changes in the agricultural support framework. The model can therefore help policymakers better assess the wider economic consequences of shocks to the agricultural sector, including an improved understanding of the geographical impacts of those shocks.